I have read a ton of views on the proposed Nigeria Tax Administration and other tax reform bills. On one hand, some stakeholders decry the bills as being a contrast to the current administration’s championing for local government autonomy. Some, like the National Economic Council (NEC), last month recommended the withdrawal of the Bills, stating that there were too many controversies surrounding it. They called for more inclusion in the stakeholder consultation process. The Northern Governors Forum (NGF) in a similar fashion rejected the new derivation-based model for Value Added Tax (VAT) distribution in the Bills. On the other hand, some wholly support the Bills and believe that its benefits are transformational and necessary. Each stakeholder and commentator holds their view in light of information that is available to them. And that is valid and fair.

But before I go into the lengthy details of my thoughts on this matter, let me share the definition of the two subjects that are crucial to this conversation: attribution and derivation.

The principle of derivation in revenue sharing ensures that revenues from taxes are distributed to the region or jurisdiction where they were generated. For example, if a company generates revenue through sales in a particular state, a portion of the taxes or royalties from that economic activity is returned to the state. The principle of attribution, on the other hand, involves allocating tax revenues based on predefined criteria, such as population size, geographical size, need, national interest, expenditure responsibilities, etc, rather than the location of a tax-generating entity. Thus revenues are collected nationally and are distributed to states according to agreed-upon formulas.

My view

The present controversy is based on the VAT-sharing formula proposed in Section 77 of the Nigeria Tax Administration Bill. I have come to appreciate that the myriad of criticisms against this well-intended bill may be a result of the lack of clarity or understanding of Section 22 (12) of the Bill, which provides for the attribution of VAT revenue, requiring companies to file their returns on the basis of derivation by location (place of consumption).

- Tax reform: For whose gain? ‘Why proposed legislations are generating controversy’

- Tax Reform Bills: Abbas, Barau must safeguard northern interests

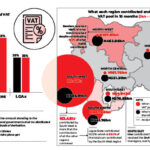

This provision, from my understanding, was included to cure an existing problem with our current VAT administration. As it stands today, in the existing system, VAT returns by companies are not filed on the basis of the place of consumption, but reported based on the head office locations of these companies. This means that a whopping 20% of VAT returns are distributed back to states where these head offices are located—whether consumption took place there or not; it explains why Lagos, FCT and Rivers always take the largest chunk of VAT under the current regime.

The proposed amendments of the Nigeria Tax Administration Bill offer a different position that emphasises fairness and a more equitable distribution of VAT returns. It proposes that VAT will now be reported based on the place of consumption, which will ensure that most of the amounts currently reported for Lagos, FCT and Rivers states will now be reported by where the consumption takes place.

The new rule will ensure that places where consumption took place get 60% of the amounts reported for them. For instance, if consumption happens in Niger State, the state would receive 60% of the VAT generated from its jurisdiction, while the balance would be put in a VAT sharing pool, which it (Niger State) would further benefit from.

In my view, this will result in a more favourable outcome for most states, when compared to the current regime that favours Lagos, Rivers and FCT. It will more or less redistribute most of the present allocation received by those 3 states.

My appeal to nec, ngf and nef as well as other stakeholders is thus:

We must not make the misjudgment of throwing away the baby with the bathing water. Let us carefully look at the benefits of these reforms and weigh the impact on our tax and fiscal space versus the proposed amendments ’‘perceived shortfalls’.

There is no single problem on earth that is without a solution. In this light, we should think out of the box and suggest workable solutions to address or fix these perceived shortfalls, or we will be condemned to having our cap in hand at the doorsteps of the World Bank and IMF Headquarters more frequently than ever.

On a personal note and based on my little experience as a tax accountant, consultant and administrator, I would suggest to all stakeholders, particularly the National Assembly to go ahead and consider the bill, pass it to law, and have Mr. President sign same, but provided the proposed amendments to the VAT law will be implemented in phases bearing in mind the following:

FIRS is currently undergoing its own reforms; the FIRS Establishment Act has been re-presented to the National Assembly and is receiving their attention simultaneously. For FIRS to be able to function as envisaged by the proposed changes or amendments to the FIRS Act, then it must first fix the roof over its head to ensure that if any storm arises tomorrow, revenue administration officials and our money entrusted in their hands would be safe.

FIRS must also fix the issue of fiscalisation within the next three to five years from now. The need for fiscalisation is one of the key amendments proposed in the Nigeria Tax Administration Bill before the NASS.

Fiscalisation is the process of using technology, like cash registers or POS systems, to ensure businesses comply with tax laws by automatically recording and reporting their sales to tax authorities.

It is an expensive project and will not only require political will at the centre but also at the sub-national level. To achieve it, the FG, FIRS and FAAC must be ready to jointly fund this project. It is important because it will bring about transparency and accountability as well as address the issue of subjectivity which is mainly the fear of the members of NEC, particularly the NGF.

I must emphasise that fiscalisation cannot happen without data. This brings me to my third point.

The FIRS HQ project should be completed, and equipped as a world-class edifice, while ensuring that the entire floor historically conceived as the “National Revenue Data Centre” becomes a reality.

Item 2 above (i.e. fiscalisation) will not only address the issue of transparency and accountability, it will curtail the influence and excesses of vested interests particularly the tax accountants who are accomplices in the whole of this VAT issue.

If the amendment is passed into law, and its implementation is not delayed say by 3 to 5 years, the fear of the stakeholders would be justified because tax accountants are likely to be subjective (or used to being subjective) in the course of filing VAT returns (i.e., VAT attribution) in favour of the states of their choice or those of the choices of some of the political class.

As a tax accountant of your company, you know where your customers are located if not all, especially the major ones. But when asked to file their companies’ monthly VAT returns based on the location of their customers, for instance, sentiments come into play. And even with the proposal in Section 77 of the Tax Administration Bill, the subjectivity is likely to continue.

Though it was an administrative initiative at FIRS in 2020, I recall that we redesigned the VAT Form 002 which required companies to file their VAT returns based on attribution. Only a few companies (less than 10) complied with our directives nationwide (i.e. file VAT returns based on the location of their customers.)

Fiscalisation will help our revenue administrators in many ways including boosting their capacity to generate more revenue for the Federation. It has the capacity to address or track transactions or sale of goods from a customer in one state to the other, particularly cashless transactions. It will also create room for the implementation of a system for immediate tax refunds.

Phasing the implementation of the two key controversial but necessary amendments to the VAT law would also assist the states to go back home, sit and weigh the level of financial inclusion in their respective states and address them accordingly. Recent reports on financial inclusion reveal that while you may have an estimated population of 10m people in a given state for example, less than 2m of that population would be financially inclusive. In some states, more than 70% of the populations do not have a BVN not to talk of a bank account. So as a state governor, your argument that huge consumption is taking place in your state but the current ‘headquarters effect’ is affecting your share of monthly VAT revenue can only be addressed when your resident population are financially inclusive. It goes without saying that your problem would be compounded in the near future if buying and selling of goods continue to happen in your state using cash. Buying and selling of goods and services in this fashion will also affect your ability to improve on your state’s IGR.

The process of input-output mechanism in VAT input claim is another key issue that has been of keen interest to me, and equally needs to be emphasized here. The intended amendments and fiscalisation of Nigeria’s business environment will also help in addressing sharp practices or the abilities of business to manipulate the input claim in the course of filing their monthly VAT returns. This is because under the current regime if an item is purchased in Lagos and taken to Kano for example, the Kano company will not be able to claim the input VAT if the Lagos company fails to correctly disclose the location of its output VAT. With fiscalisation, the input claim of the Kano company will simply expose the Lagos company.

In my view, the following four (4) factors will drive compliance of the proposed tax reform bills, and this will mean more revenue to share to the states:

Attribution is now clearly provided in the law. It is no longer an administrative decision or at the discretion of the FIRS or tax accountants working for or representing VAT agents nationwide.

There is now a strong political will to drive tax reforms; this means that tax laws will not only be passed but will be well enforced going forward in Nigeria.

Technology deployment for VAT invoicing and fiscalisation is clearly provided in the new Bills, with the attendant administrative processes that are ongoing to implement same. It will no longer be at the discretion of companies to determine who bought what—technology will.

The processes and challenges in the input-output mechanism in VAT Input claims would now be addressed using technology.

Finally, the many benefits of these bills are excellent. It behoves us to give the NASS our support to pass them into law. But I hold that we should do so on the following conditions:

- That the implementation of the Tax Administration Bill should be phased.

- That the implementation (i.e. the effective date) of the proposed amendments to Section 77 of the Tax Administration Bill should be delayed for at least three to five years to enable all parties to plan and invest in technology and the relevant infrastructure.

- FIRS should administratively prepare the minds of all stakeholders, particularly the VAT agents, lawyers and tax accountants on the need to honestly file VAT returns based on attribution as a first step because Section 26 of the FIRS Establishment Act (as it is today) is adequate enough for them to call for VAT returns based on attribution from all VAT agents in Nigeria.

- The current sharing formula should be used in distributing revenue accruable from VAT to all parties, and all parties within the next three to five years (that the amendment is expected to take effect) would have played their part so that there would be equity, transparency and accountability as intended by the proposed amendments to the VAT law.

Nami, a tax accountant and consultant, is the immediate past Executive Chairman of the Federal Inland Revenue Service (FIRS) and Joint Tax Board. He was also the President of the Commonwealth Association of Tax Administrators (CATA).

Join Daily Trust WhatsApp Community For Quick Access To News and Happenings Around You.

Join Daily Trust WhatsApp Community For Quick Access To News and Happenings Around You.